Letter to

Unitholders

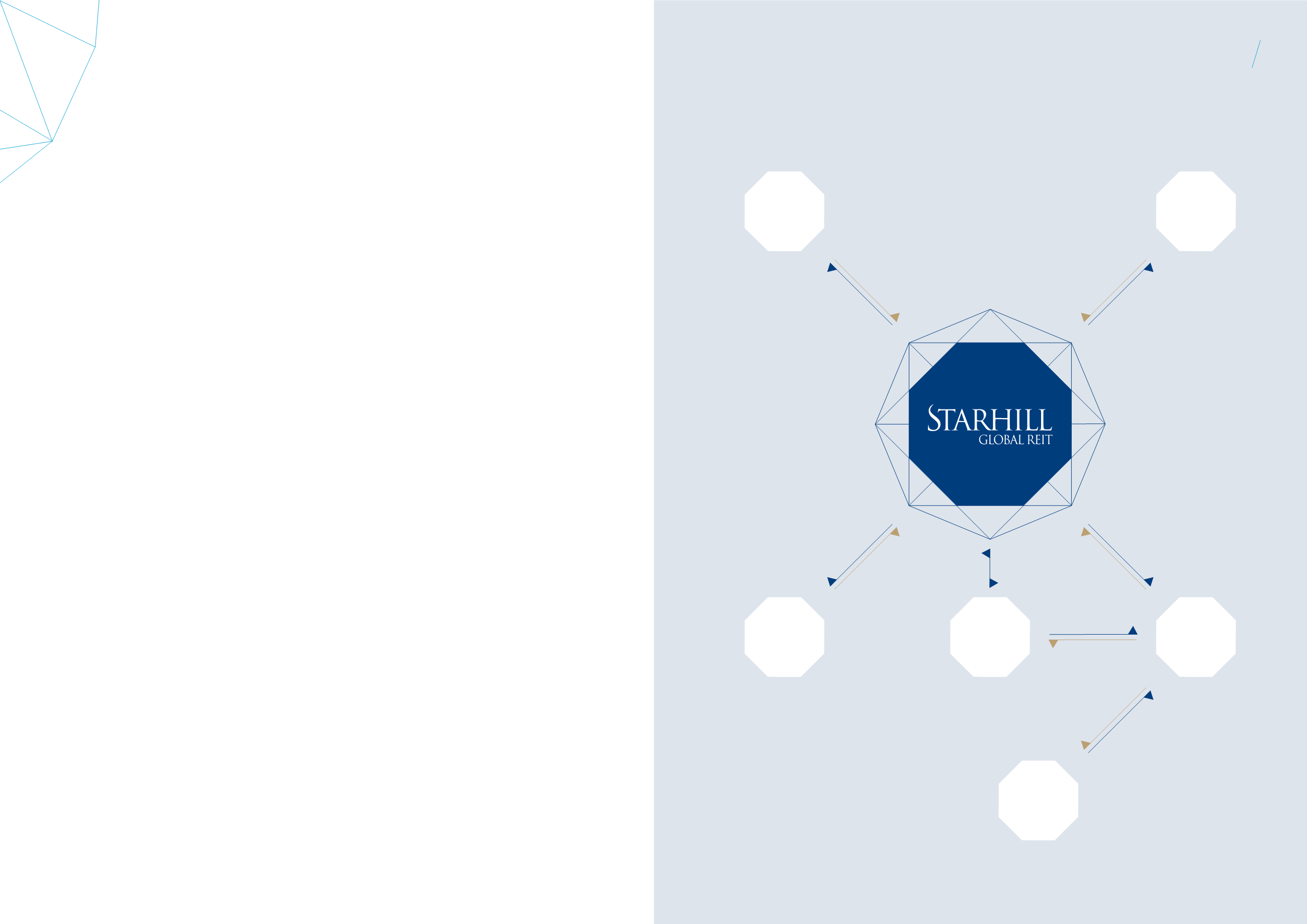

Trust

Structure

REIT

Manager

Unitholders

The

Properties

(2)

Subsidiaries

or SPVs

(3)

Property

Manager

(1)

Trustee

Hold Units

Acts on behalf

of Unitholders

Management

Fees

Ownership

of Assets

Ownership

of Assets

Property

Management Services

Distributions

Trustee

Fees

Management

Services

Net Property

Income

Net Property

Income

Property

Management Fees

borrowings, the average interest cost

of Starhill Global REIT only increased

marginally to approximately 3.2%

per annum as at 30 June 2015.

Standard & Poor’s Ratings Services

has affirmed Starhill Global REIT’s

“BBB+” rating with a stable outlook

in April 2015.

We have also been actively

refinancing existing facilities ahead

of maturities, diversifying funding

sources by tapping the bond market,

and extending the tenor of our loans

as we locked in financing cost to

mitigate interest rate exposure.

While average debt maturity

remained stable at 3.5 years as

at 30 June 2015, the maturity

profile is better staggered with

maturity being extended up to

year 2023. With the recent series of

refinancing in July 2015, there will

be no significant debt refinancing

requirement until 2018 and average

debt maturity has been extended

to approximately 4.1 years.

Starhill Global REIT derived 67.3%

(or approximately 57%

(2)

based on

full period contribution from Myer

Centre Adelaide) of the Group’s

revenue from its Singapore assets

for FY 2014/15. Foreign exchange

and interest rates environment have

experienced recent volatility. Foreign

exchange exposure for FY 2014/15

has been partially hedged via foreign

currency borrowings and short-term

foreign currency forward contracts.

As at 30 June 2015, we have also

proactively hedged all our interest

rates exposure through interest rates

swaps and caps thus mitigating the

impact of interest rates fluctuation

on DPU.

DELIVERING 10 YEARS OF

GROWTH AND PERFORMANCE

This September 2015 will mark the

10 years’ anniversary of Starhill

Global REIT since the listing on the

SGX-ST in September 2005. Over the

course of this period, the REIT has

delivered a compound annual

growth rate (CAGR) of 7.2%

(1) (3)

in DPU. Starhill Global REIT is one

of the largest REITs listed on the

SGX-ST with market capitalisation

at S$1.9 billion as at 30 June 2015,

the 13th highest amongst 32 listed

REITs. The sterling performance was

achieved due to its focus on prime real

estate. The portfolio has grown from

just S$1.3 billion solely in Singapore

to S$3.1 billion in five countries across

the Asia-Pacific with overseas assets

contributing about 33% of its revenue

for FY 2014/15. With a balanced

portfolio of master and long-term

leases as well as actively managed

leases, Starhill Global REIT has kept

portfolio occupancy at above 95%

over the last 10 years. We ended

the past 10 years having delivered

strong growth in assets and solid

performance.

LOOKING AHEAD

The International Monetary Fund’s

regional economic outlook forecasts

that growth in the Asia-Pacific area

will moderate to 5.5% next year. This

will lead to the moderation in regional

tourism and retail spending growth in

the immediate future. The prolonged

manpower crunch in Singapore may

also dampen some retailers’ plans for

expansion. The retail environment in

Chengdu remains challenging with

the ongoing austerity measures and

new supply of malls. Interest rates

and foreign exchange markets are

expected to remain volatile.

Notwithstanding the above, Asia’s

growing middle income class will

continue to underpin the longer term

retail scene. Starhill Global REIT’s

portfolio of properties in prime

locations is well-positioned to cater

to the growing pool of international

retailers seeking to establish their

presence in the region. We will

continue to refine our portfolio by

further trimming exposure of non-

core assets and selectively acquiring

prime real estate in our core cities.

We remain focused on optimising

the performance of our assets, while

leveraging on our balanced retail mall

portfolio and adopting a prudent

capital management approach, to

deliver sustainable long term returns

to Unitholders.

ACKNOWLEDGEMENTS

The Board and Management would

like to thank our directors for

their invaluable contributions and

guidance, our colleagues for their

hard work and dedication, and

our tenants, business partners and

investors for their continued trust

and support. We would also like to

thank you, our Unitholders, for your

support and confidence in Starhill

Global REIT since listing.

TAN SRI DATO’ (DR)

FRANCIS YEOH SOCK PING

PSM, CBE, FICE, SIMP, DPMS,

DPMP, JMN, JP

Executive Chairman

HO SING

Chief Executive Officer and

Executive Director

28 August 2015

Notes:

(1)

The Property Manager manages the Singapore Properties, namely

the Wisma Atria Property and the Ngee Ann City Property. The

overseas properties are managed by external property managers.

(2)

The Singapore Properties are held by Starhill Global REIT. The

overseas properties are held through its subsidiaries or special

purpose vehicles (SPVs).

(3)

The net income from overseas properties are largely repatriated

to Starhill Global REIT via a combination of trust distributions,

dividends, interest, as well as repayment of shareholders’ loans

and/or redemption of redeemable preference shares.

Notes:

(1)

The REIT’s DPUs from FY 2005 to 2Q FY 2009 have been restated to include the 963,724,106 rights units issued in August 2009.

(2)

Proforma financial effects are strictly for illustrative purposes only and were prepared based on the unaudited consolidated financial

statements of Starhill Global REIT for the 12 months ended 31 December 2014.

(3)

Excluded FY 2005 and the additional six months from January 2015 to June 2015 for FY 2014/15.

23

22

STARHILL

GLOBAL

REIT

Annual

Report

FY 2014/15